5 Steps to Take Before You Are Ready to Reapply For A Cash Loan

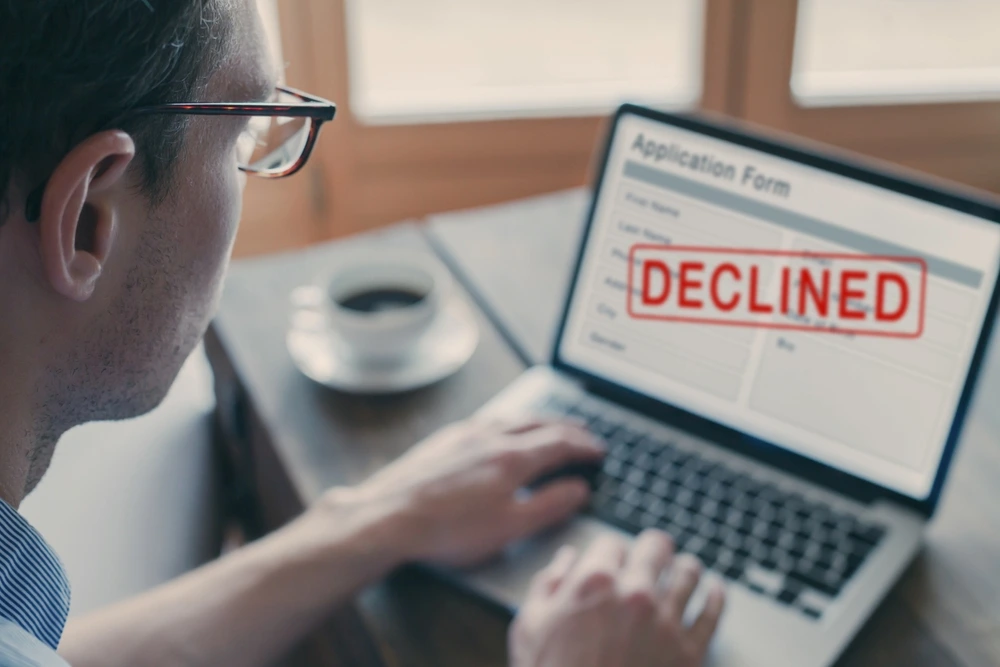

Sometimes, loan applications get rejected. It’s nothing personal, the situations between the applicant and the financial lender simply weren’t right for the loan to proceed further. It happens. We have grouped together some questions in this blog and hope to answer the overall question: what do you need to do before you are ready to reapply for a loan.

Overview:

When can you reapply for a loan?

Being rejected is disheartening especially if you had already started planning your future with that extra injection of finance. It is important to remember that a rejection of an application – for whatever reason – is simply a one-time dealing.

There is no exact time frame for when you can reapply for a loan, it all depends on your financial goals, situation and timeframe. With a few adjustments in the financial aspects of your life, you could find yourself a much more viable candidate. Swoosh has provided a 5 steps to help you work arround these issues and see when you are ready to reapply.

1. Ask yourself; has your status changed from when your application was first rejected?

Firstly, it is important not to immediately rush and ‘try again’ with another financial institution once your application is rejected. For lenders to remain profitable, they all follow stringent guidelines that will likely be similar to each others’. This means you are likely to be rejected if you don’t change your financial habits.

2. Why was your loan rejected?

Don’t give up and let your shoulders hang limp with defeat. If they haven’t explicitly stated, ask your financial institution the reason why your loan application was rejected. From there you will learn two things:

- What that lender is specifically looking for in a loan application

- How you need to align the financial aspects of your life to conform with that particular criteria.

- This is the best platform in which you can work towards making yourself a better candidate on a loan application.

3. Check credit score

Credit scores aren’t something we manually operate ourselves, so frequently reviewing them isn’t something many Australians do. Change that. It is imperative when thinking about reapplying for a loan application to do this, as your credit report will show your history of dealing with debt, and function as a lender’s main resource to determine whether you will meet your financial commitments. You can easily check your credit score for free with Equifax.

You can get one free credit report per year so use it wisely. The first time around, you may have not considered your six credit cards, excessive spending habits and late bill paying to be all that damaging to your credit score. Once you review your history, however, you could have some alarming findings that act as a much needed wake up call to reign in those harmful tendencies.

Does being denied a loan hurt credit?

Being denied a loan could hurt your credit if you’re not careful with how many loans you apply for and get rejected from. Too many unsuccessful loan applications on your credit report will be a huge red flag for the next lender to review your application, as they will say to themselves: ‘Why has everyone else said no? What are we missing? Perhaps we should think twice…’

4. Unburden yourself of unnecessary debt

When you have had too much to drink, do you sober up by ordering more tequila shots? No, that will likely result in you being ejected from the bar. You should think of your loan application and financial institutions in the same way.

If you have a series of bills sent to default, repeatedly neglect to pay your rent, and are stacking up the balance on your credit cards, then any lender will see you as unfit for a loan. As much as they would like to help, they must think of themselves first to remain a viable business, and excessive existing debt doesn’t invoke much confidence in a loan application. Before you reapply for a loan, work hard towards tightening your expenditures and covering your financial obligations in a timely manner.

Do away with wads of credit cards. Forget lavish outlays. And not just for a month or two, either. Lenders need to see an extended pattern of responsibility to consider entrusting you with their money, as loan repayments can last several months, years, and even decades. By proving you are capable and committed to honouring what you owe in other aspects of your life, then you will instantly become more favourable as a loan applicant when you decide to reapply.

5. How to get money if you can’t get a loan?

Depending on what your circumstances are, if you continue to be rejected by lenders and still trying to unburden yourself from debt, it might be wise to look at other sources of income.

Here is another Swoosh blog that can talk you through some tips for beginners trying to make money online in Australia.

Are you ready to make another application?

Have you adjusted your financial situation since your last application? Believe you are ready to meet financial commitments? Swoosh offers personal loans up to $5,000 with fixed term repayment schedules that are easy to manage within your weekly budget. For more information on how to get started, contact Swoosh today.